Seasonal carcass premiums break form

MARKET UPDATE

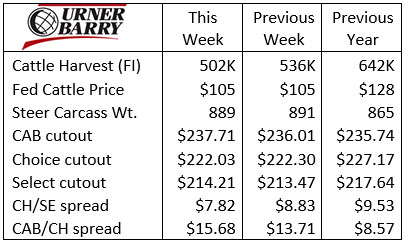

Without question fed cattle and beef sales are currently hinged entirely on the packing sector’s ability to process cattle. Throughput has not been good lately with last week’s total federally inspected (FI) head count at 502K head. That’s a 22% reduction from the same week a year ago.

Last week’s temporary closing of the JBS plant in Greeley, Colorado, was set to remain through the end of this week. The Cargill plant at Fort Morgan, Colorado, has eliminated one of two shifts per day.

So far this week the daily harvested head counts are smaller yet than last Monday and Tuesday.

Last week’s small trade volume on negotiated fed cattle yielded a $105/cwt. average, steady with the week before. Packer bids ranged widely with some bids early in the week at sub-$100/cwt. prices. Fortunately, few were sold at that level.

Packers and cattle feeders are in a bind for the moment with these weekly harvest reductions. The industry structure is an hourglass shape with the packing sector representing the narrow neck of the glass. Today the neck is exceptionally narrower than normal yet the fed cattle supply remains building in the top of the hourglass.

The boxed beef market is moving in the expected direction, sharply higher, based on the dynamics noted above. Production tonnage is greatly reduced and spot market prices reflected the change last week. Urner Barry weekly average prices (0-10 day delivery) in the table do not reflect the progressive daily price increases that occurred last week. For example, the daily Choice cutout (0-21 day delivery) advanced by about $12/cwt. Monday through Friday according to USDA. Prices continued to escalate more sharply early this week.

On a cut-by-cut basis we’re seeing a further entrenchment of the patterns established since foodservice business has been stifled. In the past month we’ve highlighted the shift in carcass value away from ribs, tenderloins, briskets and skirts in favor of several end meat cuts. Early this week boxed beef pricing indicates all-time price highs for neck-off boneless chucks, chuck rolls and chuck tenders. The same is true for inside and outside rounds as well as eyes of round. Several cuts are posting a trend reversal to the upside this week.

One must thoughtfully consider a market where the not-so-tender “chuck tender” reaches a modern-era record high price while the tenderloin trades near the BSE-induced market low seen in 1994.

Seasonal carcass premiums break form

The April fed cattle market has long been a target spring “sweet spot” for cattle feeders. This is driven by a handful of reasons, the most significant of them being that the cash market in April often brings on a price rally, marking a high for the season.

The second reason is that April is generally the beginning of larger Choice/Select price spreads and larger CAB and Prime premiums. It’s at this time that spot market middle meat sales are heating up for grilling season and with that comes a normally expanding demand signal for marbling-rich steaks.

Aggregate quality grades in the U.S. also tend to drop off significantly through late April into May. In a normal year, supply and demand factors are at odds during this period, generating some of the best premiums for high quality carcasses.

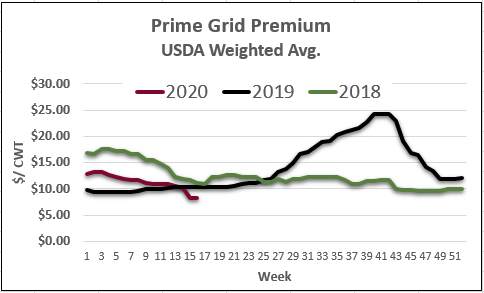

The interrupted flow of cattle and boxed beef has implications now impacting the pricing structure on a carcass value basis. The most evident change is the smaller Prime quality grade premium which has slipped to $7.71/cwt. above Choice, according to USDA’s weighted average premiums and discounts report. The Prime premium has degraded by $2.51/cwt. over the past three weeks and is down by a similar gap when compared to the same week last year. The average CAB premium in the same report slipped to $3.44/cwt. last week as well, down $1.14/cwt. in three weeks.

The reason for the degradation of these quality spreads is three-fold. First, we know that packers are currently buying fewer cattle on grid pricing arrangements. Smaller harvest capacities at packing plants have decreased the size of the weekly negotiated cash trade as well as negotiated grid cattle that packers can buy. As a result, the weighted average numbers are likely skewed toward fewer grids.

Secondly, as it relates to the Prime grade specifically, the much lower demand for rib and tenderloin subprimals has likely impacted the cutout to a large extent. Prime carcasses see the poorest utilization. Far fewer total pounds from Prime carcasses are sold specifically to fulfill Prime grade orders. The Prime premium degrades quickly as price quotes move away from middle meats even though this has improved in recent years.

Finally, carcass marbling measurements at the current time are fractionally higher than a year ago. This means we’re seeing record percentages of Choice and Prime grade carcasses this spring even though the tonnage total in all grades is significantly smaller.

The Choice/Select price spread is behaving at or above the level that we’d expect in April with a $12.22/cwt. premium in last week’s report. This means that all Choice and higher grade carcasses priced on a grid at this time will still see a decent cumulative premium.

The above factors are enough to illustrate some dynamics that are currently affecting the premium structure of value based carcass sales now and in the immediate near term. These short term fluctuations are to be expected, especially when considering the enormity of changes that have impacted the beef supply chain.

The many challenges the beef market is facing today are serious short term problems but are not indicative of long term trends. Price and demand signals will also realign as the pandemic subsides.

Innovations arise in foodservice

New trends are emerging in food sales around the country in the wake of restricted options. The restaurant sector has been a big source of media coverage, with countless stories describing restaurants that have closed indefinitely to restaurants that have re-established their business creatively. Still, many in the foodservice segment have experienced furloughs or staff reductions.

Innovative ideas have cropped up in the foodservice sector with many examples coming from brand partners across the country. While restaurants transitioned to take-out and delivery, many have partnered with third-party delivery companies, created special menus highlighting dishes that are ideal for takeout, or created many “take and make” items, allowing customers to be the chef while the restaurant provides the items and instructions.

The foodservice distribution sector of the beef supply chain is one that receives perhaps the least focus as we think about the “gate to plate” story. However, this extensive list of vital companies have also been hamstrung by the foodservice downturn. Distributors have also had to be nimble in the ever-changing landscape. Many distributors have opened their warehouses to the public, offering drive-through product pickup on designated days. They have also established pop-up shops with restaurant customers, creating a unique opportunity for consumers to get their hands on some higher quality meat and unique cuts they might not be able to get at their local retail store. Some distributors are working with local neighborhood organizations as well, setting up shops in local business parking lots, church parking lots and more.

DON’T MISS THE LATEST HEADLINES!

Make AI work for your herd

New lens on animal welfare

Fueling your cows

Don’t wince

Read More CAB Insider

$100,000 Up for Grabs with 2024 Colvin Scholarships

Certified Angus Beef is offering $100,000 in scholarships for agricultural college students through the 2024 Colvin Scholarship Fund. Aspiring students passionate about agriculture and innovation, who live in the U.S. or Canada, are encouraged to apply before the April 30 deadline. With the Colvin Scholarship Fund honoring Louis M. “Mick” Colvin’s legacy, Certified Angus Beef continues its commitment to cultivating future leaders in the beef industry.

Carcass Quality Set to Climb Seasonally

With the arrival of the new year the beef market will rapidly adjust to changes in consumer buying habits. This will remove demand pressure from ribs and tenderloins, realigning the contribution of these most valuable beef cuts to a smaller percentage of carcass value

Misaligned Cattle Markets and Record-high Carcass Weights

Few things in cattle market trends are entirely predictable but the fact that carcass weights peak in November is as close to a sure bet as one could identify. Genetic selection for growth and advancing mature size has fueled the long-term increase in carcass weights.