Restaurants pivot to survive, retailers can’t keep up

MARKET UPDATE

Beef market conditions in the past two weeks have responded with tremendous force in the wake of COVID-19 as U.S. consumer buying at retail escalated to a frenzy. Fear of food shortages is a very real phenomenon for the public, as shoppers come face to face with empty meat cases. When food supplies appear scarce then the momentary reality is that they are scarce. This behavior has driven retail beef clearance to a heightened degree.

In the meantime U.S. Federally Inspected (F.I.) beef production continues at record pace with an incomprehensible 6% year-to-date increase over 2019. Just to be clear, this is the largest volume in history.

Back to the market, boxed beef values have skyrocketed beginning mid-March with USDA (0-21 day delivery) and Urner Barry (0-10 day delivery) showing the daily spot market Choice cutout value advancing 25% or 15%, respectively. By comparison, the USDA Choice cutout spiked 12% following the Holcomb plant fire last August.

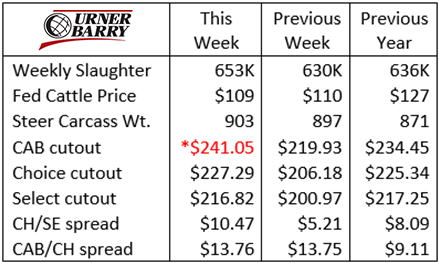

Last week’s CAB cutout price is listed with an asterisk in today’s table to highlight the fact that this is reported on Thursday whereas Choice and Select are reported through Friday. The abrupt daily price movement last week was such that a one-day difference in reporting creates a discrepancy in the averages that needs to be noted. As such, the CAB cutout value should read a few cents higher on the week.

The other side of this predictable response in boxed beef values is the lack of a similar spike in fed cattle prices. CME Live Cattle futures contracts have been closely aligned with equity markets, following the downward trajectory seen in equity index values since late February. As boxed beef prices moved sideways during the first week of March, followed by the recent spike, the April LC contract moved down from a $120/cwt. price point on February 20th to the contract low $92/cwt. last Friday, March 20th.

Plenty of commentary can be written in the margins but cash fed cattle prices have shouldered more than their share of negativity through the futures, reflecting a different picture than the daily beef supply and demand dynamics.

A small light of hope was seen late last week as more than one packer chose to increase the week’s negotiated prices established earlier in the week. By Tuesday this week the market is reflecting the same with $115/cwt. live bids on small volume. Live Cattle contracts were up the limit Monday and Tuesday but mostly negative Wednesday with the only positive being the April contract, up just over $3/cwt. by midday.

Restaurants pivot to survive, retailers scramble to keep up

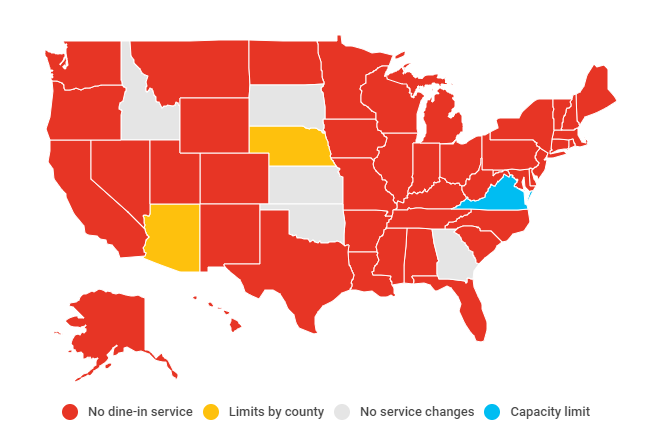

The biggest shift in U.S. food business today is the sudden and absolute shock to the restaurant (foodservice) sector as establishments are forced to cease dine-in operations. RestaurantBusinessOnline.com features a map showing that all but 8 states have mandated “no dine-in service” policies while 3 of the remaining have county by county policies or capacity limits.

Foodservice companies have cancelled, turned back or reduced orders greatly as the reality of these policies have taken hold. Undoubtedly, many will not survive the financial strain. Still others are pivoting to hang on with take-out meals and reimagined menus to fit shelter-at-home mandates.

On Tuesday this week a coalition of restaurants asked U.S. consumers to participate in “The Great American Takeout” in an effort to gain consumer support and awareness of the challenge that restaurants are now facing.

With so many people facing “stay at home” orders, food delivery has become a focal point for restaurants previously not offering that option. On a restaurant by restaurant basis it’s clear that some will survive on take-out and delivery while other establishments will not.

As so much beef has been displaced from the foodservice sector retailers have run out of beef and other proteins in their meat cases. With weekly beef volume at all-time highs it’s not a matter of enough beef to go around, there’s plenty to feed everyone. The problem that retailers face today is getting enough in the store as consumers stock up not for a week or two, but possibly a month’s worth of beef. The beef industry infrastructure is simply struggling to keep up with the “right now” demand at grocery stores.

Our team here at Certified Angus Beef LLC has been lending support to licensed partners at both retail and foodservice through this changing landscape as best we can. One example of a “win” in the supply chain comes by way of Buckhead Toledo and Sysco Pittsburgh. Normally suppliers to the foodservice industry, these companies stepped out to provide 400 cases of CAB product recently to Giant Eagle grocery stores to fulfill their needs.

The accompanying photo from the brand’s partner, Giant Eagle in Rocky River, Ohio, depicts an empty meat case with CAB product available in “cut to order” format due to exceptional shopper demand.

Similarly, some foodservice distributors have adapted to sell “protein bundles”, in a sense pivoting to selling wholesale cuts directly to consumers. Del Monte Meat Company in California recently partnered with restaurant customers to create variety packs of meat- their Steak and Chop box featured Certified Angus Beef ® brand NY strips and ground beef. As of a week ago, they had sold 3,000 bundles. Similarly, many restaurants have rebranded themselves into temporary markets, selling not only protein they had on hand, but also dry goods, produce and even, in some cases, cleaning supplies and the ever elusive roll of toilet paper. Many in the foodservice industry have been adape during this trying time in order to stay afloat.

End meats, grinds up big at retail

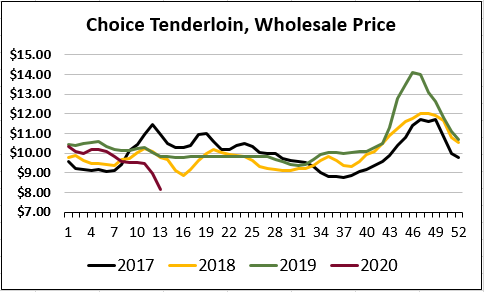

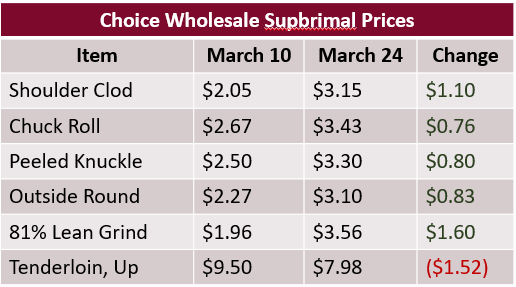

Stepping away from the bifurcated beef/cattle market for a moment, let’s look at the carcass subprimal price impact as beef supply shifts volume toward retail. We’ll use commodity Choice pricing since price points are reported daily and thus most current.

With almost every item showing price gains in the past several days it’s clear that beef, in total, has seen significant inflation. Yet some might be surprised to learn that the Choice tenderloin has devalued by $1.52/lb. in a matter of 14 days beginning at $9.50/lb. on March 10 to $7.98/lb. this Tuesday. The tendency toward higher value for the tenderloin at fine dining restaurants becomes clear given today’s circumstances. Who would have thought it possible for tenderloins to be 13% cheaper when the Choice cutout is higher by more than 20%? The CAB tenderloin price is down $0.15/lb. in the latest two weeks, but this week’s data will publish tomorrow with that update.

Subprimal cuts that have inflated the most are less surprising. With all of the demand boom at retail we’ve seen end meats gain the most. Some of the main cuts with the largest increases are shoulder clods, chuck rolls, peeled knuckles, inside and outside rounds as well as ground beef. Many of those large-end meat subprimals will see their way to the grinder in the grocer’s meat department to fulfill ground beef demand.

It would seem that the panic buying may subside some as consumers either see meat case supplies restocked or simply gain some confidence in their personal food security. We’re in uncharted territory but suppliers up and down the chain are doing their level best to keep beef moving toward the proper outlets.

DON’T MISS THE LATEST HEADLINES!

BQA creates confidence

Building the best

Rising to the occasion

Blog: This too shall pass

Read More CAB Insider

Credit End Meats With CAB Value-Add

We focused on fourth-quarter middle meat demand as a beef price driver in the last edition of the Insider. This is certainly the case in the current data as rib and tenderloins are pricing near their annual highs. However, a look at annual price trends across the beef carcass shows increasing contributions to CAB premiums from both ends of the carcass.

Middle Meats and Supply Driving Fourth Quarter Spreads

At the retail level, November brings a brief shift in focus, away from beef to turkey and ham, for Thanksgiving meals. Turkeys are the classic “loss leader” item in grocery stores during November as retailers practically give them away to lure a volume of shoppers to spend on the high-margin center of the store goods.

CAB Brand Sales Third Best in 45-Year History

In this CAB Insider,shifting market dynamics have already marked trend changes in the 2023 cattle and beef markets. These shifts are most succinctly summarized through two factors, fewer cattle and higher prices, that will further entrench themselves in near term trends.