Carcass quality set to increase

MARKET UPDATE

In the past two weeks, the beef supply chain has remained under extreme pressure, with packing plants undergoing varying degrees of both worsening and recovering states of workforce health. Plants that experienced trouble early on in the pandemic timeline seem to be slowly recovering, while those unaffected in the beginning stages are currently undergoing their biggest challenges.

In the last CAB Insider we focused on the temporary closure of the JBS plant in Greeley, Colorado. This was a shock to many of us, but in the ensuing time several plants have dealt with closures ranging from two days for cleaning, to two weeks for more widespread personnel health concerns and testing.

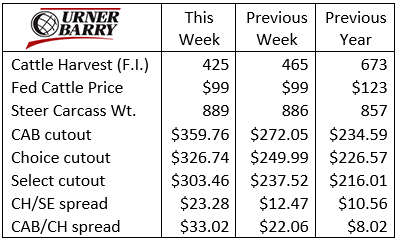

The beef and fed cattle markets continue to pass along ugly results. Last week’s negotiated fed cattle trade saw a wide range in prices with the top side reported at $105/cwt., live weight, with the bottom as low as $90/cwt.

The backlog in fed cattle is going to be a “new normal” for quite some time as several examples are reported with cattle already a month behind schedule from their optimal shipping date. Carcass weights are slightly higher in the USDA reports, well above historical seasonal trend lines.

The boxed beef complex in the past two weeks has seen prices in an unprecedented inflationary pattern as the bottleneck tightens. Keeping up with boxed wholesale pricing is a daily need for buyers at this point whereas a weekly update would have sufficed during normal product movement conditions.

Focusing on the daily Choice spot market cutout is the bellwether of the largest volume of fed cattle product sales. As of Tuesday this week, the Choice cutout was $4.22/lb., 53% higher than two weeks ago.

Product quality price spreads are dramatic while availability is extremely limited. The Choice/Select spread had advanced to $0.33/lb. early this week according to USDA, well above the weekly average reported in the table. The CAB/Choice spread is similarly extreme and most likely advancing above recent quotes.

End meats continue to lead the charge in terms of the year-over-year increase in spot market prices. However, middle meats and briskets which were almost hard to give away a few weeks ago have posted serious trend reversals as retailers are now seeing their beef orders shorted on tight supplies.

Carcass quality set to increase, conformity challenged

Diminished packing capacity will generate a set of beef statistics for 2020 like no other year. Likewise, pushing fed cattle back to later ship dates has several implications that will change the product mix.

Feedyards can do little to substantially slow the daily gain for their cattle on feed. Foregoing beta-agonists in the feeding regime is the first, most obvious tactic deployed by many feeders who had shipping dates pushed back. Some have discussed limit feeding to slow gains, but bunk space has to be ample enough that each animal has room to eat simultaneously for this to work. This is rarely the setup when filling a feedlot pen so it’s a non-starter for most. Some feeders are considering changing to maintenance diets to slow weight gain with implications to cost of gain posing further financial challenges.

Richer marbling and higher subsequent quality grades, on average, will result from more time on feed and added age. While overfeeding isn’t a recommended strategy to achieve higher quality grades, it is one consequence of current supply chain dynamics.

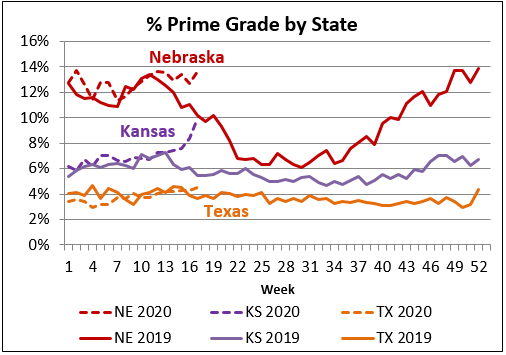

Northern packers are seeing their Prime grade rates jump to the upside with the national Prime grade average up to 10.7% of the mix. Kansas firms saw the most aggressive change with a 3 percentage point (ppt.) increase in Prime carcasses in the past 7 weeks. Normally the Kansas grade would be dropping quickly into April, as it would be across the packing sector.

There are no knobs to turn or levers to pull that will boost enough CAB product supply for end users while fed cattle harvest is around 60% of normal volume at CAB-licensed packing plants. Higher marbling rates will push more carcasses into the brand from one perspective, but other brand specifications will likely create obstacles despite predicted richer marbling.

Carcass weights are already creating issues for several shipments of cattle at the kill floor as the 1,050 lb. maximum threshold for the brand is surpassed. The big steers also carry more risk for ribeye sizes above 16 sq. inches. Finally, the extra feeding days will push some animals over the 1-inch maximum backfat requirement for the brand.

The unfortunate and inevitable downside is the yield grade 4 and 5 rates for the month of April and beyond will be much higher than normal, certainly much higher than the 12% yield grade 4 rate reported in March.

It is, however, most important not to miss the forest for the trees as we discuss cattle and product flow through the supply chain. The challenges presented now are very important to cattlemen and brand partners up and down the chain. However, the health of people at the packing level and throughout the country is the priority that must receive full focus and priority.

Competing proteins update

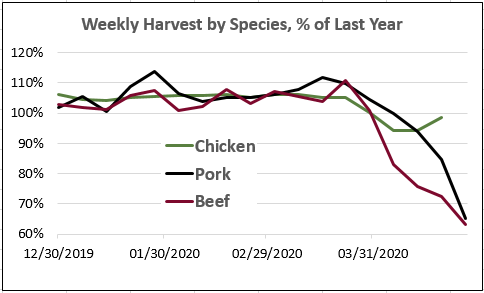

Impacts from COVID-19 are shared across all the major U.S. protein packing sectors, as pork and poultry processing have also been sidelined. Record 2020 production volumes projected at the beginning of the year were coming to fruition early but have been waylaid for all major animal proteins.

Weekly U.S. hog harvest has slowed at an increasing rate with last week’s 1.55 M head a mere 55% of the total just six weeks earlier. Disappearance of restaurant demand had driven the pork cutout from a healthy $0.79/lb. in late March to a devastatingly low $0.54/lb. by the second week in April.

Another price reversal came swiftly as most recent processing cutbacks have sent the pork cutout to $0.94/lb. based on scarcity of supply. Wholesale loin prices have reached well beyond historical spring highs while bellies are now just back to a seasonal norm.

Weekly chicken production has declined the least, just 13% from late March through early April. Throughput has improved in the last week with the total head count now just 9% off from the spring high.

Currently chicken parts vary greatly depending on their normal demand at foodservice. Jumbo wings, for instance, have struggled to find buying demand as their normal sports bar consumption venues were shuttered. Drumsticks, on the other hand, have increased from $0.32/lb. to $0.42/lb. for fresh, spot market product. Chicken breasts are 22% cheaper in the weekly spot trade than a year ago at this time, likely hit by smaller customer traffic at quick-serve and dine-in restaurants.

DON’T MISS THE LATEST HEADLINES!

Keep cattle antibiotics working

A Rare Breed

The Resistance Part I: Works today, not tomorrow?

The Resistance Part II: The bacteria battle

Read More CAB Insider

$100,000 Up for Grabs with 2024 Colvin Scholarships

Certified Angus Beef is offering $100,000 in scholarships for agricultural college students through the 2024 Colvin Scholarship Fund. Aspiring students passionate about agriculture and innovation, who live in the U.S. or Canada, are encouraged to apply before the April 30 deadline. With the Colvin Scholarship Fund honoring Louis M. “Mick” Colvin’s legacy, Certified Angus Beef continues its commitment to cultivating future leaders in the beef industry.

Carcass Quality Set to Climb Seasonally

With the arrival of the new year the beef market will rapidly adjust to changes in consumer buying habits. This will remove demand pressure from ribs and tenderloins, realigning the contribution of these most valuable beef cuts to a smaller percentage of carcass value

Misaligned Cattle Markets and Record-high Carcass Weights

Few things in cattle market trends are entirely predictable but the fact that carcass weights peak in November is as close to a sure bet as one could identify. Genetic selection for growth and advancing mature size has fueled the long-term increase in carcass weights.