CAB carcass specifications expanded

MARKET UPDATE

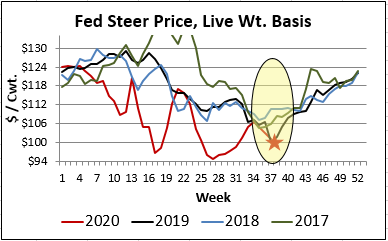

The past two weeks have brought more weakness in the cash live cattle market. After touching the $106/cwt. mark in mid-August, the upward momentum was lost. Last week’s trade saw prices dip by $1 to $2/cwt., even though Live Cattle futures had a fairly positive week, premium to the cash market.

As we look at historical seasonal tendencies, there’s plenty of argument that the market is behaving exactly as it should. Regardless of the 2019 fall market irregularities and this year’s backlog, recent years seasonal trendlines show prices finding annual low right around the current timeframe.

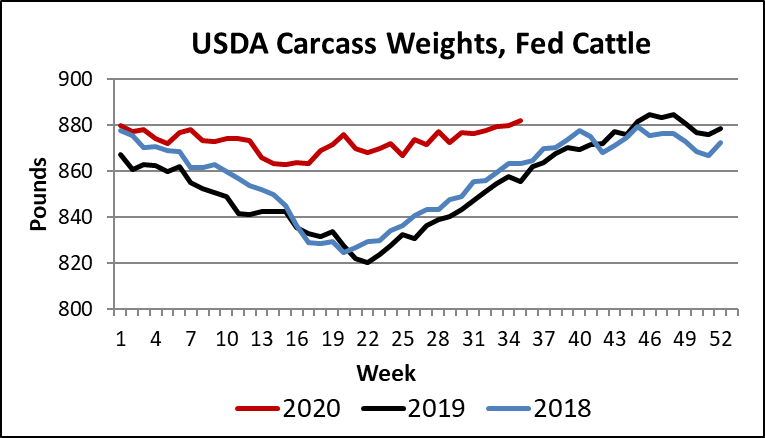

Fall is quickly approaching, and that brings on the annual carcass weight increase, climbing up the normal annual November peak.

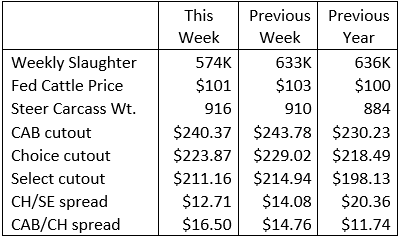

As shown in the table, the most recently reported 916-lb. average weight for a steer carcass is 32 lb. heavier than a year ago. That’s certainly not helping to keep beef tonnage in check even on smaller total harvested numbers. Also bear in mind last week’s holiday-shortened harvest schedule doesn’t compare well with the same week a year ago since Labor Day fell on the prior week in 2019.

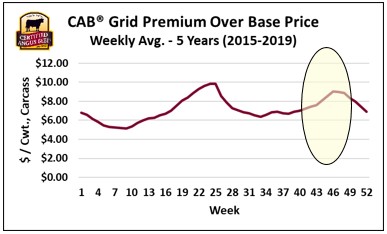

Carcass cutout values continue to follow expectations as well, with September weakness a strong seasonal trend. Fourth-quarter price increases normally follow, and we’ll make no prediction here to argue against it.

Quality spreads remain decent although this Tuesday’s CH/SE spread narrowed to $8.65/cwt. on negotiated sales. The CAB cutout last week was a very stout $16.50/cwt. above Choice.

CAB Carcass Specifications Expand

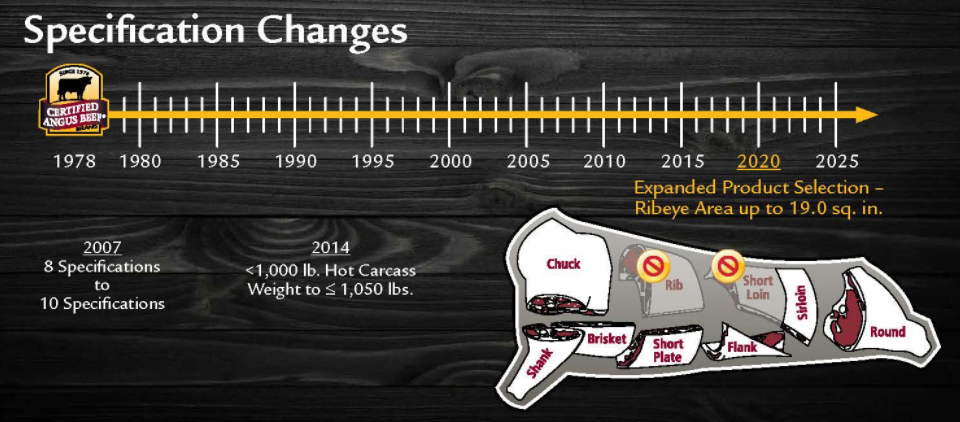

In the Certified Angus Beef ® brand’s 42-year history there have been precious few alterations to the 10 carcass specifications that have built demand and consumer confidence in the brand.

In 2007 the decision was made to remove Yield Grade as a singular specification, replacing it with three stand-alone components of the Yield Grade formula.

In 2014 industry evolution to heavier live-animal and carcass weights prompted a move from the 1,000-lb. hot carcass-weight maximum to a new ceiling of 1,050 lb. These changes were calculated and customer outcomes were heavily considered in the process. These decisions have proven to be the “right call” in hindsight, for cattlemen and consumers alike.

The brand recently announced two additional carcass spec modifications to further enhance opportunities for stakeholders.

The first is more technical in nature, limiting carcasses accepted by the brand to “1 inch or less” external backfat thickness, rather than the previous verbiage of “less than 1 inch.” This move helps provide graders more clarity in the era of camera-assisted grading where computers measure backfat to several decimal places.

A footnote seems appropriate regarding backfat thickness.The brand’s Production Team does not recommend 1 inch of backfat thickness as a target. Rather, focusing on a mark closer to 0.6 inches has been shown to optimize CAB acceptance rates in combination with economically sound percentages of Yield Grade 4 carcasses.

The second change allows packers with an extended licensing agreement to box beef from carcasses that meet all quality specifications, but exceed the ribeye area, up to 19 square inches. Ribs, ribeyes, strip loins and short loins from these carcasses will be excluded from the brand. The traditional 10-16 sq inch ribeye spec remains to maintain sizing and consistency of middle meats.

Several end meats and cuts remaining from the loin primal are not negatively impacted by large ribeye area measurements. In fact, end users will likely be pleased to find greater availability of some items, such as briskets, during periods of smaller cattle supplies. Some cuts are also more desired in larger sizes, unlike those important middle meats for steak and roast applications.

Fourth quarter grid marketing challenge

As we ease toward October, feedyard managers will remain hopeful for increasing values in both cash cattle and deferred live cattle futures contracts. Alongside those aspirations, quality-focused managers start to consider widening carcass quality price spreads as holiday buying demand begins in mid-October.

Feedyard managers have dealt with heavy cattle all summer and as we head toward November’s peak of annual carcass weights, they’ll have their hands full. We’re seeing carcass weights creep higher, so those smaller spring placements aren’t pulling average carcass weights down at this time.

Cattle managers will likely need to do more sorting through the fall and into winter if they want to capitalize on anticipated larger fourth quarter carcass quality premiums. Managers will have decisions to make regarding the risk/reward proposition. Premiums for Choice, CAB and Prime carcasses will need to be greater than the risk associated with discounts for heavy carcasses and Yield Grade 4’s and 5’s.

DON’T MISS THE LATEST HEADLINES!

Prevention and preparation pay

Breeding for the brand

The market demands more demand

Brand specifications evolve

Read More CAB Insider

Credit End Meats With CAB Value-Add

We focused on fourth-quarter middle meat demand as a beef price driver in the last edition of the Insider. This is certainly the case in the current data as rib and tenderloins are pricing near their annual highs. However, a look at annual price trends across the beef carcass shows increasing contributions to CAB premiums from both ends of the carcass.

Middle Meats and Supply Driving Fourth Quarter Spreads

At the retail level, November brings a brief shift in focus, away from beef to turkey and ham, for Thanksgiving meals. Turkeys are the classic “loss leader” item in grocery stores during November as retailers practically give them away to lure a volume of shoppers to spend on the high-margin center of the store goods.

CAB Brand Sales Third Best in 45-Year History

In this CAB Insider,shifting market dynamics have already marked trend changes in the 2023 cattle and beef markets. These shifts are most succinctly summarized through two factors, fewer cattle and higher prices, that will further entrench themselves in near term trends.