CAB carcass cutout premiums bolstered

MARKET UPDATE

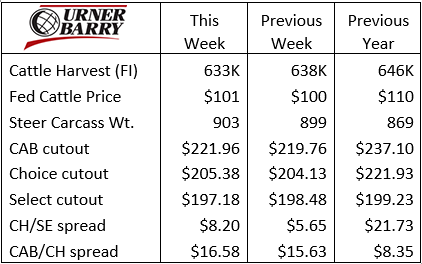

The fed steer and heifer market keeps working toward normalized levels, but at a very slow pace. Last week’s $101/cwt. steer price was roughly a dollar higher than the week prior. That marked five straight weeks of higher prices, yet remained $9/cwt. lower than a year ago.

Since the dismal summer low of $95.34/cwt. the week of July 6th, marginal increases were seasonally “on time” in the two weeks following. Still, the five-week upward price trend has been heartening to cattle feeders and producers at the front of the supply chain.

The Iowa/Minnesota region continued to report the top of the price range from $103 to $105/cwt. last week. Show lists in the northern tier of the main feeding region hint at a more current finished-cattle inventory. That development has spread a bit toward the west as well, with some trade in western Nebraska at $103/cwt. last week.

The boxed beef market strengthened last week with retailers buying for Labor Day in the early August spot market. The CAB cutout value was up $2.20/cwt. last week, with Choice boxes up $1.25/cwt. Select grade carcasses are just 14% of the total fed cattle carcass mix, compared to almost 19% a year ago. Yet the Select cutout slipped lower by $1.30/cwt. last week. Demand centers on Choice as the baseline but the CAB/Choice spread was a hearty $16.58/cwt. in the latest spot-market data, versus $8.35/cwt. a year ago.

A closer look at individual CAB carcass cuts will show ribeyes emerging from their summer price low, allowing rib primals to reflect the most upward price movement last week. The loin primal brought mixed price direction with strip loins, ball tips and short loins cheaper than a year ago and strips also trending lower. Tenderloins were trending higher but still below a year ago, thanks to to seasonality and lack of significant foodservice demand.

The round primal saw firmer prices across the board but, as noted, the overall carcass cutout shows prices below a year ago and ripe for buying. Chuck items were mixed last week but the balance shows the chuck primal relatively steady.

Inside skirts and flank steaks were priced near their 2019 values while lower prices on CAB whole-muscle grinds should be a draw for large retail volume.

CAB Carcass Cutout premiums bolstered

Spot market carcass cutout values are subject to anomalies. Protein buyers may take advantage of opportunities in seasonal shifts, market disruptions or other unexpected changes in supply and demand.

Modern technology lets buyers acquire more of the desired beef cuts at a bargain and “deep freeze” them for resale much later. Advanced freeze and thaw techniques allow those cuts to be offered at retail with the same look and eating attributes as fresh product. Consequently, buyers can lay in a greater volume of a given item when prices are low, eventually selling at higher prices in a season when consumer demand and prices are on the rise.

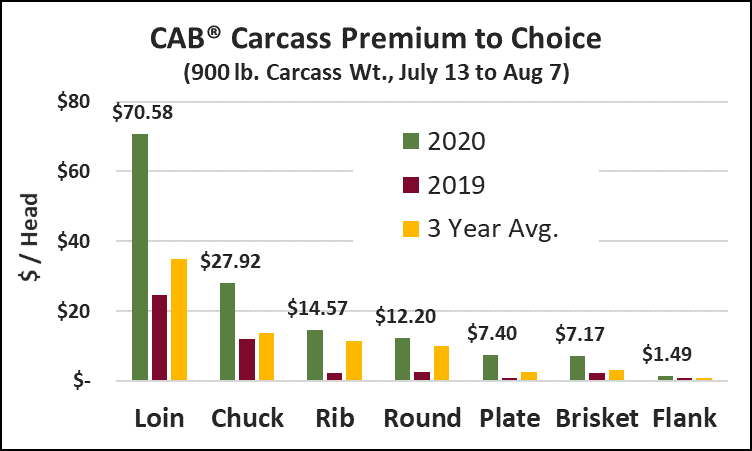

A combination of these factors may be affecting the current CAB loin cutout value in relation to Choice. The bar chart shows the latest four-week average CAB carcass premium above Choice, broken down into the contribution of each primal.

The loin primal normally leads when it comes to total premium dollars contributed by each carcass primal through the CAB label. The loin can make up 21% of bone-in carcass weight, carrying the premium strip and tenderloin cuts that enjoy a nice CAB markup over Choice. CAB tri-tips, top sirloins, ball tips and sirloin flap meat carry a smaller premium, but still help increase the total loin premium.

The latest data for CAB peeled tenderloins shows a $1/lb. premium above Choice tenderloins. It’s more normal, seasonally, for that price spread to be about 40¢/lb. The fact that foodservice business in 2020 is far below historical norms also suggests there may have been some large buys taking place for the “deep freeze” scenario, as tenderloins spent much of the summer notably discounted compared to last year. The dynamics don’t add up, so it’s sensible to consider that some large retailers may have already made tenderloin purchases to store until winter holidays.

The total carcass view over the past four weeks shows a robust CAB premium over commodity Choice. The green bars in the accompanying chart indicate larger year-over-year spot market premiums, bolstered across the carcass. The recent trend is similarly exaggerated, compared to the past three-year averages.

Each subprimal contributes to the premium depending on the percentage of carcass weight the primal represents, plus the premium per pound. Even as the total loin premium is much larger than a year ago, the percentage contribution is slightly lower in that comparison.

Notably higher than a year ago in the ranking are ribs, rounds and plates, in relation to the total carcass premium.

Calf prices, breakevens and grid values

As we near mid-August, many cow-calf operators are starting to look at what the market holds for calves this fall. Some have weaned calves early or are considering doing so because of drought conditions.

Live Cattle (LC) futures have been trending higher since July 20th for the April and June 2021 contracts. This is building an optimistic scenario for cattlemen looking to sell calves that will exit the feedlot as finished next spring. The cost of corn in the low $3/bushel range is keeping a lid on feedlot cost projections, and low interest rates are favorable, too.

Breakeven projections using June 2021 LC indicate a 550-lb. steer delivered in early October may be priced right at $152/cwt., allowing for interest and 150 miles of freight to the feedlot. Calves in this weight range may not go directly on feed, however, as many are being purchased for more than that $152 breakeven to be backgrounded cheaper through the winter.

The larger, 650-lb. steers will likely go straight on feed for an April or May finish. Today’s April 2021 LC contract is at a $6.68/cwt. premium to June, allowing the heavier steer to pencil a breakeven purchase price close to $154/cwt. for October delivery.

Including carcass value in the feedlot’s projections is a hedge that pushes buyers to pay a little more for the very best calves. High-carcass-quality cattle may achieve 50% CAB and 10% to 20% Prime. Managing finish dates to mitigate yield grade 4s and heavy carcasses enters the equation as well.

Few feeders will spend much time calculating potential grid returns in their projections. Instead, experience and seasonal market tendencies provide an estimated added value. Conservative, yet high-percentile estimates for carcass quality on a generic grid calculation suggest $6/cwt. carcass premiums would be easy enough to pencil. This figures out to a premium of nearly $7/cwt. at the time of purchase for the 650-lb. steer and $9/wt. for the 550-lb. steer.

DON’T MISS THE LATEST HEADLINES!

FQF coming to you

Free registration for FQF webinar

Cultivated curiosity

Read More CAB Insider

$100,000 Up for Grabs with 2024 Colvin Scholarships

Certified Angus Beef is offering $100,000 in scholarships for agricultural college students through the 2024 Colvin Scholarship Fund. Aspiring students passionate about agriculture and innovation, who live in the U.S. or Canada, are encouraged to apply before the April 30 deadline. With the Colvin Scholarship Fund honoring Louis M. “Mick” Colvin’s legacy, Certified Angus Beef continues its commitment to cultivating future leaders in the beef industry.

Carcass Quality Set to Climb Seasonally

With the arrival of the new year the beef market will rapidly adjust to changes in consumer buying habits. This will remove demand pressure from ribs and tenderloins, realigning the contribution of these most valuable beef cuts to a smaller percentage of carcass value

Misaligned Cattle Markets and Record-high Carcass Weights

Few things in cattle market trends are entirely predictable but the fact that carcass weights peak in November is as close to a sure bet as one could identify. Genetic selection for growth and advancing mature size has fueled the long-term increase in carcass weights.